Contents:

- What Is Compound Interest?

- Difference Between Simple and Compound Interest

- Benefits of Compound Interest

- Potential Pitfalls and Misconceptions

- How Does Compound Interest Impact Savings Accounts?

- How Does Compound Interest Impact Investments?

- How Does Compound Interest Impact Pensions?

- How Does Inflation Impact Compound Interest?

- How Do Taxes Affect Compound Interest?

- How Can I Take Advantage of Compound Interest?

1. What Is Compound Interest?

Compound interest refers to the interest calculated on the initial principal, which also includes all the accumulated interest from previous periods on a deposit or loan. It is like earning interest on interest. This is what sets it apart from simple interest, where interest is calculated solely on the initial amount, or principal, you invest or borrow.

Here's an example: Imagine you have £1,000 in a savings account in a bank, and it earns an annual interest rate of 5%. Here's how compound interest would function:

Year 1: You'll earn £50 in interest (5% of £1,000), making your total £1,050.

Year 2: You'll earn £52.50 in interest (5% of £1,050), making your total £1,102.50.

Year 3: You'll earn £55.13 in interest (5% of £1,102.50), making your total £1,157.63.

As you can see, each year, you earn interest on the new total, not just the original £1,000. This leads to increasingly larger interest amounts each year, resulting in an exponential growth curve.

Compound interest is an integral part of various financial products. It impacts savings accounts, investments, pensions, and loans. Understanding how it works can help you make informed decisions about your finances.

- Savings and Investments: Compound interest can turn small, regular savings into a

significant sum over time. It's a core concept in the investment strategies of many US and UK-based

financial

institutions and private investors.

- Loans and Mortgages: Conversely, when it comes to loans or mortgages, compound interest can increase the overall amount you'll have to pay back. Being aware of this can guide you in managing your debts more efficiently.

Our compound interest calculator is designed to help you understand how your savings, investments, and debt obligations might grow over time.

2. Difference Between Simple and Compound Interest

Understanding the difference between simple and compound interest is vital for making informed financial decisions. These two concepts may seem similar, but they operate on different principles, and their impact over time can be quite distinct.

Simple Interest

Simple interest is calculated solely on the principal amount or on that part of the principal amount which remains unpaid.

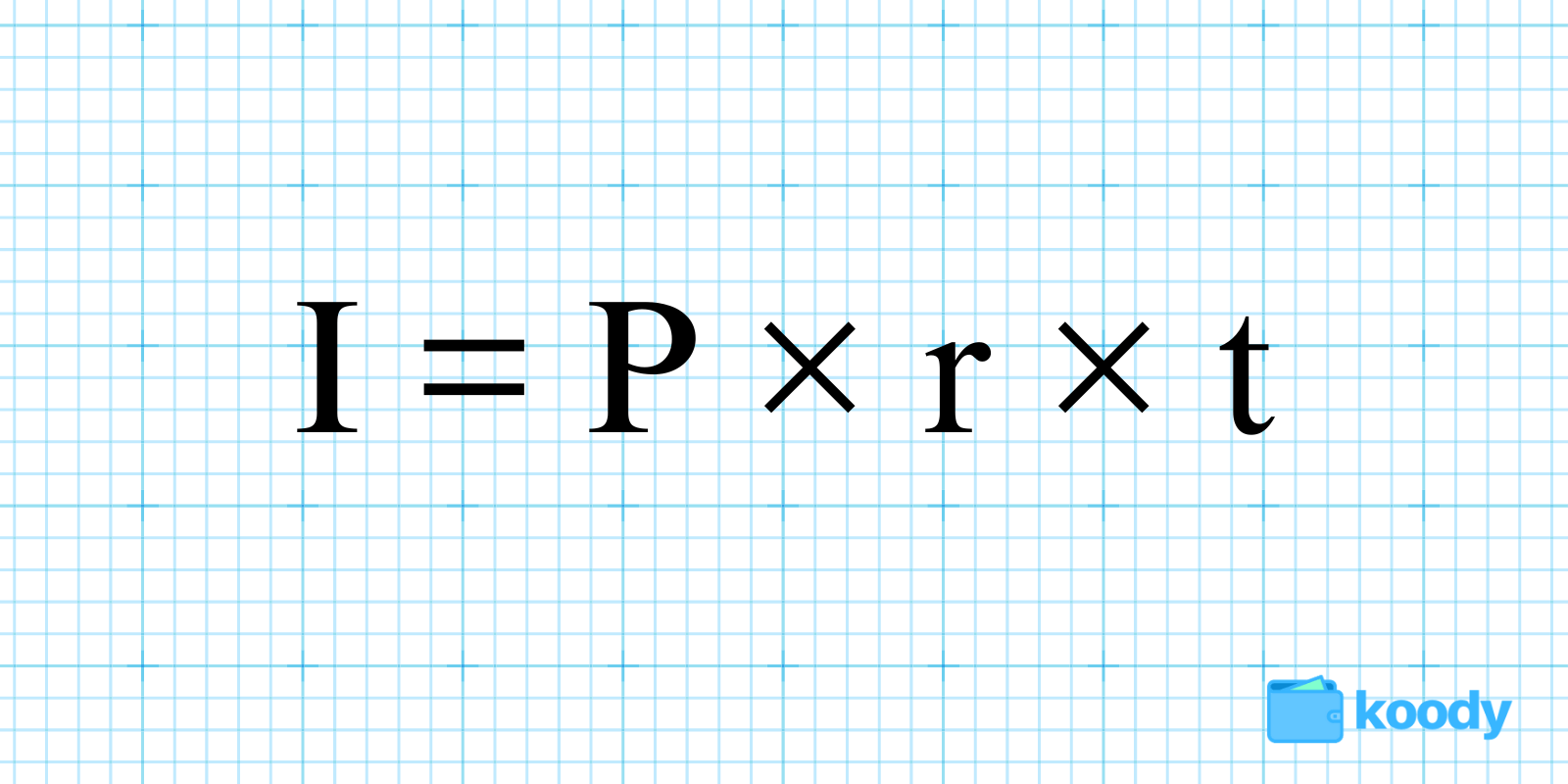

The formula for calculating simple interest is:

Where:

- I is the interest

- P is the principal amount

- r is the annual interest rate

- t is the time in years

In the UK, simple interest might be applied to some short-term loans or investment products. Here's an example to illustrate how simple interest works:

- Initial Principal: £1,000

- Annual Interest Rate: 5%

- Time Period: 3 years

Using the formula, the total interest over 3 years would be £150, and the total amount after 3 years would be £1,150.

Compound Interest

Compound interest is the interest calculated on the initial principal and also on all accumulated interest from previous periods.

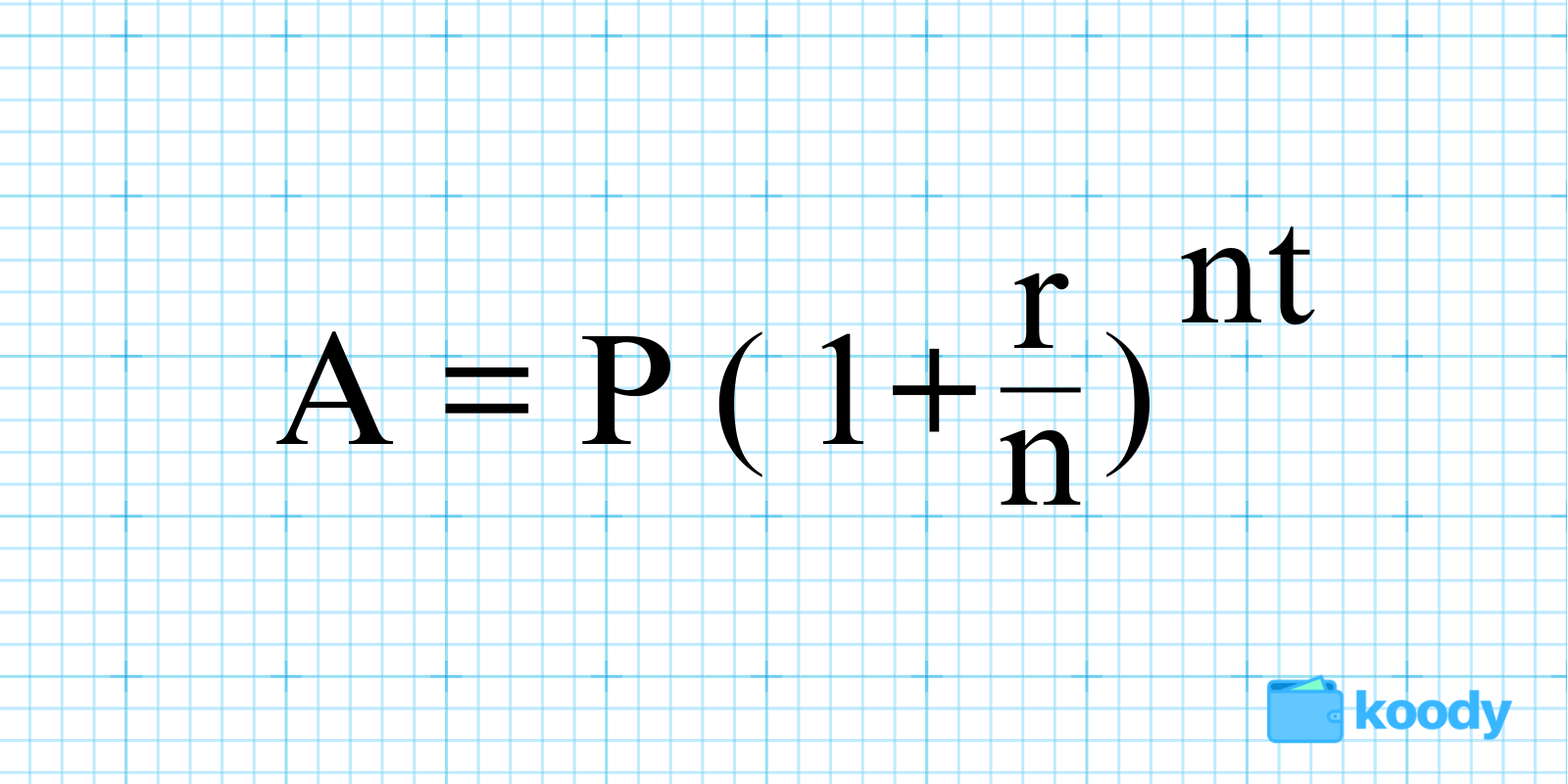

The formula for calculating compound interest is:

Where:

- A is the amount of money accumulated after "n" years, including interest

- P is the principal amount

- r is the annual interest rate (in decimal)

- n is the number of times that interest is compounded per year

- t is the time the money is invested or borrowed for (in years)

Here's an example:

Let's say you invest £1,000 at an annual interest rate of 5%, compounded yearly, for 3 years. Using the formula, you can calculate the future value of the investment as follows:

This means that after 3 years, the investment would grow to approximately £1,157.63. You can use our compound interest calculator above to visualise your investment growth over time.

Key Differences

- Interest Calculation: Simple interest is calculated on the principal only, while

compound interest

includes interest on both the principal and the accumulated interest.

- Growth Over Time: Compound interest leads to exponential growth, whereas simple

interest leads to linear

growth. In the long run, compound interest can result in significantly higher returns or costs.

- Common Usage: In the UK, simple interest might be more common in short-term financial products, while compound interest is often applied to long-term savings, investments, and loans.

3. Benefits of Compound Interest

Compound interest has been described as the "eighth wonder of the world" by some financial experts, and for good reason. Its exponential growth potential offers numerous benefits that can significantly affect personal and institutional finances. Here's a closer look at the advantages of compound interest, particularly within the UK financial context.

- Exponential Growth: Compound interest has the power to multiply wealth exponentially,

providing growth not only on the initial investment but also on previously earned interest. This

continuous reinvestment leads to an increasingly steep growth curve, especially over extended

periods.

- Encourages Saving and Investing: The magic of compound interest works best over time.

The longer the money is invested or saved, the greater the compound effect. This can motivate individuals

to save or invest their money rather than spend it, promoting a culture of financial responsibility and

planning.

- Enhances Retirement Savings: For UK residents planning for retirement, compound

interest can be an essential ally. By investing in pension funds or other retirement vehicles that benefit

from compound interest, individuals can build substantial nest eggs that will provide financial security

in their later years.

- Facilitates Achieving Financial Goals: Whether it is buying a home, paying for

education, or going on a dream holiday, compound interest can help you achieve your financial goals. By

strategically choosing savings or investment products that capitalise on compound interest, you can reach

your targets faster and with less initial capital.

- Can Be Tailored to Individual Needs: In the UK, financial institutions offer various

products that utilise compound interest, with differing frequencies of compounding (e.g., daily, monthly,

annually). This flexibility allows individuals and businesses to choose options that align with their risk

tolerance, financial goals, and time horizons.

- Mitigates the Effects of Inflation: In an economy where inflation is a concern, compound interest can help preserve the purchasing power of money. By earning interest on interest, savers and investors can potentially outpace inflation, protecting the real value of their capital.

4. Potential Pitfalls and Misconceptions

Compound interest is a powerful financial tool, but it is not without its challenges and potential misunderstandings. Here's an overview of some common pitfalls and misconceptions associated with compound interest.

Pitfalls

- High Compounding on Debts: While compound interest can grow savings exponentially, it

can have the opposite effect on debts. For those in the UK with loans or credit card balances subject to

compound interest, unpaid balances can grow rapidly, leading to a spiral of increasing debt.

- Over-Reliance on Compound Interest: Some individuals might misunderstand how compound

interest works and over-rely on it for financial growth without considering other factors like investment

risk, market conditions, or individual financial needs.

- Impatience with Slow Initial Growth: Compound interest typically shows modest growth in

the early years and then accelerates. A lack of patience or understanding of this curve might lead some

people to withdraw their money early, missing out on the exponential growth in later years.

- Neglecting Fees and Taxes: Compound interest doesn't account for potential fees, taxes, or other deductions that might apply to an investment or savings account. Ignoring these factors can lead to a distorted view of the actual growth.

Misconceptions

- Equating Compound Interest with Guaranteed Growth: Compound interest doesn't guarantee

success or growth. Market volatility, poor investment choices, or economic downturns can offset the

benefits of compounding.

- Misunderstanding Compounding Frequency: The frequency with which interest is compounded

(daily, monthly, annually) can greatly affect the total return. Misunderstanding this aspect may lead to

unrealistic expectations.

- Thinking All Investments Compound Equally: Not all investment or savings products in

the UK use compound interest, and even those that do might have different terms and conditions. Assuming

that all products will compound equally can lead to misplaced financial decisions.

- Underestimating the Importance of Initial Contributions: While compound interest plays a significant role, the amount initially invested or saved is equally crucial. Relying solely on compound interest without making regular or sufficient contributions may lead to disappointment.

5. How Does Compound Interest Impact Savings Accounts?

Compound interest greatly affects how savings grow in the UK. Let's explore both Cash ISAs and Standard Savings Accounts:

- Increased Growth Over Time: A Cash ISA with an annual interest rate of 2% compounded

monthly would grow a £5,000 deposit to about £6,100 in

five years, assuming no additional deposits. This

growth would be tax-free in the UK.

- Incentive to Save: A Standard Savings Account with a similar interest rate and

compounding frequency might encourage a saver to leave the funds untouched, allowing the compound interest

to work its magic.

- Variety of Choices: Different banks and building societies in the UK offer a range of Cash ISAs and Standard Savings Accounts with varying interest rates and compounding frequencies, enabling savers to choose options that suit their financial goals.

6. How Does Compound Interest Impact Investments?

Investments like Stocks and Shares ISAs and Lifetime ISAs can benefit significantly from compound interest:

- Long-Term Growth Potential: Investing £10,000 in a Stocks and

Shares ISA with an

average annual return of 5% and reinvesting all dividends would grow to approximately £16,386 in 10

years.

- Strategic Planning: Investors might choose funds or stocks within their Stocks and

Shares ISA that pay dividends, using those dividends to purchase additional shares, thus compounding the

growth.

- Balancing Risk and Reward: By understanding how compound interest works, UK investors can make informed decisions about risk and reward within their ISAs, balancing high-growth stocks with more stable bonds, for example.

7. How Does Compound Interest Impact Pensions?

In the UK, Self-Invested Personal Pensions (SIPPs) provide flexibility and the potential for growth through compound interest:

- Enhanced Retirement Wealth: A person investing £200 per month

into a SIPP with an

annual return of 6% compounded monthly could expect their pension to grow to approximately £349,101 over

30 years.

- Benefit of Time: Starting a SIPP at age 30 instead of 40 could mean tens of thousands

of pounds more in retirement, thanks to the compounding effect.

- Informed Decisions: By choosing different assets within a SIPP, such as stocks, bonds, or real estate, you can tailor your pension growth. Understanding how compound interest works in each asset class can guide these decisions.

8. How Does Inflation Impact Compound Interest?

Inflation refers to the rate at which the general level of prices for goods and services rises, eroding the purchasing power of money. While compound interest can lead to the exponential growth of savings or investments, inflation can offset some or all of this growth. Let's discuss the nuances:

1. Reduction in Real Returns

Example: If a Cash ISA in the UK offers a 3% annual interest rate compounded annually, and inflation is running at 2%, the real return on the savings is only 1%. A £10,000 deposit would grow to £10,300 nominally in a year, but its purchasing power would only be equivalent to £10,100 in the previous year's money.

2. Impact on Fixed Income Investments

Fixed-Rate Bonds and Savings: The value of fixed-rate bonds or savings accounts might be particularly vulnerable to inflation. If inflation surpasses the fixed interest rate, the real return could be negative.

Example: A 5-year fixed-rate bond in the UK with an annual interest rate of 2% would lose real value if inflation averaged above 2% during the same period.

3. Implications for Retirement Planning

SIPPs and Pension Funds: The effect of inflation on compound interest is a vital consideration for retirement planning. Inflation can erode the real value of pension funds over time, even if they are growing nominally.

Example: A UK resident contributing to a SIPP that grows at 5% annually but faces an average inflation rate of 3% must consider this 2% real growth rate when planning for retirement.

4. Variable Interest Rate Products

Adjusting to Inflation: Some investment and savings products in the UK might offer variable interest rates that adjust with inflation, mitigating its impact.

Example: Inflation-linked bonds, whose interest payments rise with inflation, can provide a hedge against losing purchasing power.

5. Long-Term Considerations

The Erosion of Wealth: Over the long term, even modest inflation can significantly erode the real value of savings and investments that are compounding at a rate below or near the inflation rate.

Example: A 30-year investment in the UK compounding at 2% annually would lose considerable purchasing power if inflation averaged 3% over the same period.

9. How Do Taxes Affect Compound Interest?

Taxes can significantly shape the growth of compound interest. Various factors such as income tax, capital gains tax, and dividend tax can either boost or hinder the compounding effect. It is essential to note that the examples provided below do not consider individual tax allowances and exemptions, which can further impact the real rate of compound growth. Understanding these elements can guide more effective financial planning.

1. Tax on Interest Income

Standard Savings Accounts: Interest earned in standard savings accounts is subject to income tax in the UK. This tax can reduce the effective interest rate, slowing the compounding effect.

Example: If you're in the 20% tax bracket, a savings account offering 3% interest would effectively yield only 2.4% after taxes.

2. Tax-Efficient Accounts

Individual Savings Accounts (ISAs): ISAs, including Cash ISAs and Stocks and Shares ISAs, allow interest and investment returns to compound tax-free. This can lead to more substantial growth over time.

Example: Investing £5,000 in a Stocks and Shares ISA with a 5% return would grow to £8,144 in 10 years, tax-free. The same investment in a taxable account might grow to only £7,700 after taxes (assuming a 20% tax rate).

3. Tax on Dividends

Reinvested Dividends: If you reinvest dividends outside of tax-efficient accounts like ISAs, those dividends are typically subject to tax. This can lessen the compound growth of the investment.

Example: A dividend yield of 3% on an investment might effectively be 1.9875% after a 33.75% dividend tax, reducing the compounding effect.

4. Capital Gains Tax

Selling Investments: Realising gains by selling investments outside of tax-efficient accounts can trigger capital gains tax, reducing the funds available for reinvestment.

Example: Selling shares that have appreciated by £1,000 might result in £800 after a 20% capital gains tax, reducing the amount that can be reinvested and compounded.

5. Tax on Pension Growth

Self-Invested Personal Pensions (SIPPs): Contributions to SIPPs are usually tax-deductible, and growth within the pension compounds tax-free. However, withdrawals may be subject to income tax.

Example: A SIPP growing at 6% annually would compound without tax impact until withdrawal. Depending on your tax bracket at retirement, a portion of the withdrawals might be taxed.

6. Inheritance Tax Considerations

Passing on Wealth: The compounding effect can significantly grow wealth, but inheritance tax considerations may affect how that wealth is passed on.

Example: Proper planning with trusts or other estate planning tools in the UK might mitigate inheritance tax, preserving the compounded growth for beneficiaries.

10. How Can I Take Advantage of Compound Interest?

To take advantage of compound interest in the UK, you'll need to:

1. Start Early and Invest Regularly

Example: By starting a Stocks and Shares ISA at age 25 instead of 35, with monthly contributions of £200 and an average annual return of 6%, you could have an additional £100,000 or more by retirement.

Pitfall to Avoid: Procrastination can result in significant lost growth.

2. Understand Your Savings and Investment Options

Example: Selecting a Cash ISA with a competitive interest rate and regular compounding (e.g., monthly) could result in higher returns compared to a Standard Savings Account.

Pitfall to Avoid: Be cautious of accounts with higher rates but less frequent compounding or hidden fees that might reduce the effective interest rate.

3. Reinvest Dividends and Interest

Example: In a Stocks and Shares ISA, reinvesting dividends rather than taking them as cash can exponentially increase the value over time.

Pitfall to Avoid: Ensure that reinvesting aligns with your risk tolerance and overall investment strategy.

4. Contribute to a Pension Fund like a SIPP

Example: Regular contributions to a well-diversified Self-Invested Personal Pension (SIPP) can leverage compound interest to build a significant retirement nest egg.

Pitfall to Avoid: Investing too conservatively within your SIPP may lead to growth that fails to outpace inflation.

5. Utilise Tax-Efficient Accounts like ISAs

Example: Contributions to a Cash ISA or Stocks and Shares ISA in the UK are free from income and capital gains tax, maximising the compounding effect.

Pitfall to Avoid: Be mindful of annual contribution limits to avoid penalties.

6. Monitor Inflation and Adjust Strategy

Example: Consider inflation-linked bonds or other assets that might protect against inflation's erosion of real returns.

Pitfall to Avoid: Diversify investments to avoid overexposure to any one asset, including those linked to inflation.

7. Maintain a Long-Term Perspective

Example: Staying committed to a consistent investment strategy over many years can lead to substantial compound growth, even if individual investments fluctuate in the short term

Pitfall to Avoid: Reacting emotionally to short-term market changes can lead to decisions that hinder long-term growth.